A brief review of how much life insurance you may need

Life insurance responds to the uncertainty of financial stability if death or serious illness were to happen. For many, it can be the big elephant in the room…Something that should be addressed for the wellbeing of yourself, family, and/or employees, but it can be difficult to think about, and look intimidating to figure out.

September is almost over, and since it is Life Insurance Awareness Month, Mosaic Insurance Alliance wanted to do a sequel to our Common Life Insurance Myths blog from earlier this month. Below are some basic life insurance tips accompanied by a life insurance calculator that can help you determine how much protection you might need.

We all have a finite amount of time here, though most of us don’t know what it will be. Anything can happen to anyone. Others in our lives are affected when we pass on, and there are times where the policy holder may need to use the financial support from their life insurance policy for themselves prior to passing—chronic, critical, and terminal illnesses happen more often than you might think. You most likely know somebody with a chronic or critical illness—cancer, paralysis, major organ failure, Alzheimer’s, dementia, heart attack, and stroke to just name a few…Chronic and critical illness are the leading cause for bankruptcy, as well as the leading cause of small business failure, in the U.S.

An Important Note to Keep in Mind:

Most typical life insurance policies only pay out money to the beneficiaries (usually a spouse or family) if the policyowner dies, but that doesn’t have to be the case—you can get a life insurance policy with living benefits. However, it is also important to know that most of the policies that have “living benefits” are for terminal illness only. There are only a select few of life insurance companies that have “full living benefit” policies which cover terminal, critical, and chronic illness. It can get a little confusing, but that is what we are here for! We would be more than happy to answer any of your questions and help you get the coverage that you specifically need. Our lives are all different, and Mosaic can help you determine what you need based on different life variables that make you, you. We can be reached at: info@mosaicia.com or 425-320-4280.

The Two Main Types of Life Insurance:

Type 1: Permanent Life Insurance:

This type of life insurance is guaranteed to pay out whether you leave this earth in one year, or when you are 101 years old and counting. When you have permanent life insurance, you pay a premium that is fixed when you take out the policy in return for that assured payout. It can be thought of as a partial form of saving, which will probably have a residual value if you decide to discontinue the policy.

With a permanent life insurance policy, your premium will always be the same, though higher than you would pay for a similar term policy. With a permanent policy, you and your dependents will always have the comfort of knowing they will be provided for. Additionally, since the benefit is guaranteed, your policy can be used as a collateral for a loan.

Type 2: Term Life Insurance:

As the name suggests, a term life insurance policy will pay out to your dependents if death occurs during an agreed period—usually 10-15 years. After the agreed period, the policy lapses. As with permanent life insurance, term life insurance policies have a fixed premium. The main difference with the fixed premium is that with term insurance, it is solely for the current term of the policy. Also, keep in mind that if you were to cancel a current term life insurance policy, you will probably have no refund.

Since term life insurance policies do not pay if the policy expires before you pass away, term life insurance premiums are cheaper than permanent life insurance premiums. Term policies tend to be well-suited for covering the expensive periods of your life when you are on a tight budget—such as when you are raising a family or paying a mortgage.

However, an important factor to highlight is that with a term policy, you are not building up any savings like with a permanent policy. So, when your term expires, taking out a new policy will cost you substantially more than the previous one because you will be older.

There are different plans to fit different needs, and one plan may be better for you than another. We can help you determine which plan is best for you.

After You Choose Your Plan…

After you decide on which life insurance plan is best for you, an insurer will generally require you to take a medical examination. They most likely will also ask you details of your health and that of your parents. This helps them calculate the risk that they are covering. In a few cases—where the benefit is quite low or if the policy has a moratorium on paying out in the first couple of years—this requirement may be waived.

Is Life Insurance Necessary?

“That will never happen to me” may not always be the case. Things can happen to anyone and the future is not absolute. Life insurance helps you create a safety net for all that you hold dear. But, yes, there could be circumstance where you might deem life insurance as currently unnecessary for you. For instance, if you have a significant savings to sufficiently meet all the foreseeable needs of you and your dependents, you might not find it feasible to get a policy for the time being. You should discuss this with a financial advisor.

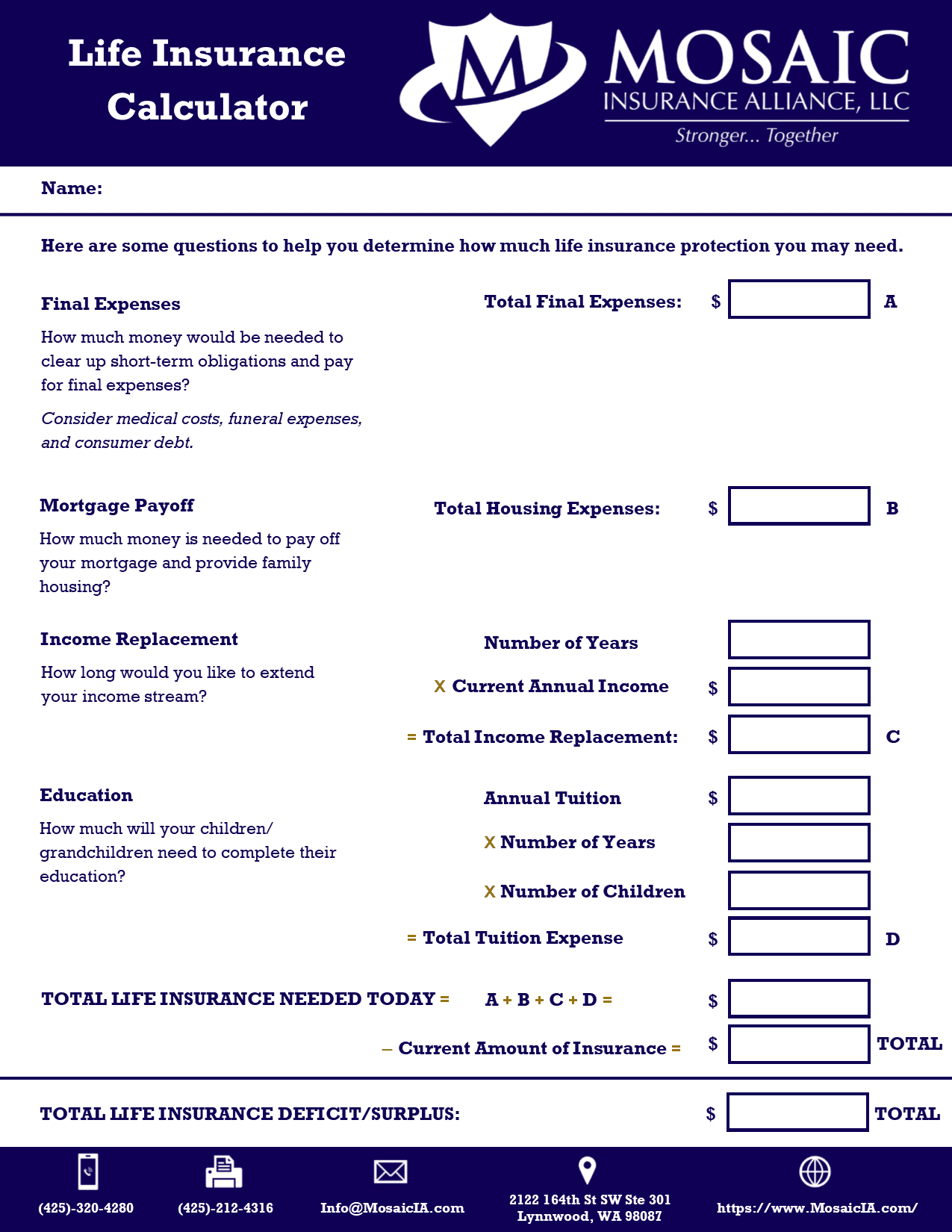

So, should I get life insurance? A good start to answering this question is to set out your current financial commitments and needs, against any life coverage you may already have, to get an idea if there is a gap you need to fill. To help you do this, we encourage your to do the simple life insurance calculator worksheet below.

Life Insurance Calculator

You can print out the below life insurance form here.

Life Happens also has a great life insurance calculator. If you have any questions at all, don’t hesitate to call or email us! We look forward to talking to you.